Holidays can bring joy and happy memories, but they also can mean problems ahead for your credit scoreif you find yourself: – Running up balances. Here are four strategies to protect your credit— and one time when putting a temporary dent in your credit score is worth it.

1. Watch your balances

Your credit card spending probably goes up around the holidays, not just from buying gifts, but also due todecorating, entertaining and perhaps traveling to be with family.

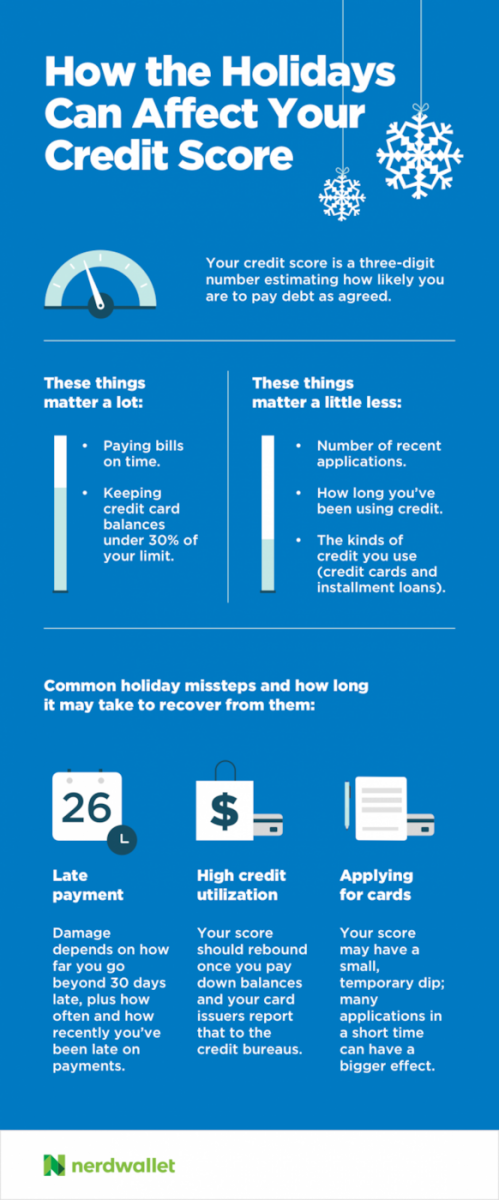

Higher balances can mean lower credit scores, because credit utilization— how close your balance is to your limit — plays a major role in the scoring systems. “If your credit utilization ratio rises to about 30% or so, you can expect to see your credit score drop,” says NerdWallet credit card expert Sean McQuay, “and that effect gets more pronounced the more debt you carry.” This can happen even if you pay in full each month. If your card issuer’s monthly report to the credit bureaus happens before your payment is credited, a high balance will show up — and hurt.

Good news: The damage is temporary. Your score should recover within three months if you consistently pay your bill on time and whittle balances back down, says credit card expert and author Beverly Harzog. As long as you don’t plan to apply for credit soon, she says, don’t worry about that temporary dip in your score. If you do plan to apply for credit soon,consider avoiding high utilization at any point in your billing cycle by making more than one payment amonth.

2. Say ‘No, thanks’ to store cards

When a sales clerk cheerily asks if you’d like to save 20% on your purchases today, it’s smart to smile back and say, “No, thanks.” Store cards tend to have high interest rates, making them an expensive way to shop. And they often have low credit limits, so even a small balance can mean high credit utilization. Getting a retail card makes sense only if you plan to shop regularly at that store and the card offers useful discounts or bonuses. “But you go into a relationship with a retail card with the promise that you’ll never carry a balance,” Harzog says. 3. Use reminders to avoid latepayments

Staying on top of bills during this busy time can gettricky. Overflowing mailboxes may mean your bill gets lost between pages of a sale flier. When you pull out a rarely used card or sign up for a new one, you may overlook the unfamiliar bill that shows up much later. A late payment fee is bad enough, but paying more than 30 days late will really bruise your credit because payment history has the biggest influence on your score. The negative mark can stay on your credit report for up to seven years, although the impact fades over time. Check outthe tools your card issuer offers as part of its online account access. You may be able to set text or email alerts to remind you of due dates, warn when you’re approaching a credit utilization level you choose and more. You may also want to set calendar reminders and make a note about which cards you’ve used. “The more unorganized you are, the more likely you are to make a mistake,” Harzog says.

4. Check it twice, for fraud

It’s wiseto go online at least once a week to check your credit card accounts for charges you didn’t make, Harzog says. Consider checking even more often in the holiday season, when fraud traditionally rises. Keep an eye on online purchases in particular. Embedded EMV chips are making it harder to make counterfeit cards, so criminals are focusing their efforts on online shopping and other ways to purchasewithout a physical card. The sooner you discover a problem, the sooner you can undo the damage. Know when a drop in your score is worth it

It’s good to build and safeguard your credit, but don’t let it get in the way of a financial move that’s right for you.

Harzog gives 0% balance-transfer cards as an example. If you’re paying interest on a credit card but have excellent credit, you could save by opening a 0% card and consolidating high-interest debt onto it. You may see a small ding from applying for credit, then a dent from bumping up close to your credit limit as you gather high-interest debt onto one card. But over the long term, paying off credit card debt as cheaply as possible puts you in a better financial position. And that’s what really counts. Bev O’Shea is a staff writer at NerdWallet, a personal finance website. Email: boshea@nerdwallet.com. Twitter: @BeverlyOShea. The article 4 Ways You Can Protect Your Credit Score Over the Holidays originally appeared on NerdWallet.

– Applying for a store credit card without a plan.

– Making latepayments.

– Falling victim to fraud.

4 Ways You Can Protect Your Credit Score Over the Holidays